Non Occupant Co Borrower Freddie Mac – For experienced borrowers and investors, I decided to post a comprehensive comparison chart between Fannie Mae and Freddie Mac. The chart shows the difference in the ‘lending criteria’ required for the loans purchased by the two companies.

Keep in mind that some of the lending rules are not set in stone and will change over time. As a lender, you must understand and stay current on new rules and regulations to continue to initiate, fund, and successfully close escrows. Some people may find this information useful, others may learn something new.

Non Occupant Co Borrower Freddie Mac

The middle column displays the sections, while the left and right columns display the differences between the credit standards required by Fannie Mae and Freddie Mac, respectively. Not all loans are created equal…

Freddie Mac Targeted Affordable Housing Express Loans

Fannie and Freddie are important. They are government-registered corporations (“government-sponsored entities,” or GSEs) with limited corporate powers, such as financing single-family homes and multifamily homes. They are publicly traded companies with private shareholders. Both are great. At the end of 2000, Fannie had assets of $675 billion. Freddie had $459 billion. At the time, when ranked by resources, they were the third and fifth largest “private corporations” in the United States.

The Federal National Mortgage Association is commonly known as Fannie Mae (abbreviated “FNMA”). It was founded in 1938 during the Great Depression. It is actually a Government Sponsored Enterprise (GSE) and went public in 1968. The primary purpose of the creation of FNMA was to expand the secondary mortgage market by securing loans in the form of mortgage-backed securities (MBS). MBS allowed lenders to refinance assets for cash and increased the number of lenders in the housing market. FNMA has also reduced its reliance on second-hand goods and loans. FNMA does not provide loans directly to consumers or homebuyers.

Federal Home Loan Mortgage Corporation is commonly known as Freddie Mac (abbreviated as ‘FHLMC’). It was established in 1970 to further expand the secondary market for religious buildings in the United States. It is also a Government Sponsored Enterprise (GSE). With loans purchased on the secondary market, Freddie Mac recognizes them as collateralized debt securities and sells them to investors on the open market. This secondary mortgage market increases the amount of money available, making more money available for mortgage loans and new home purchases. Freddie Mac does not provide loans directly to consumers or homebuyers.

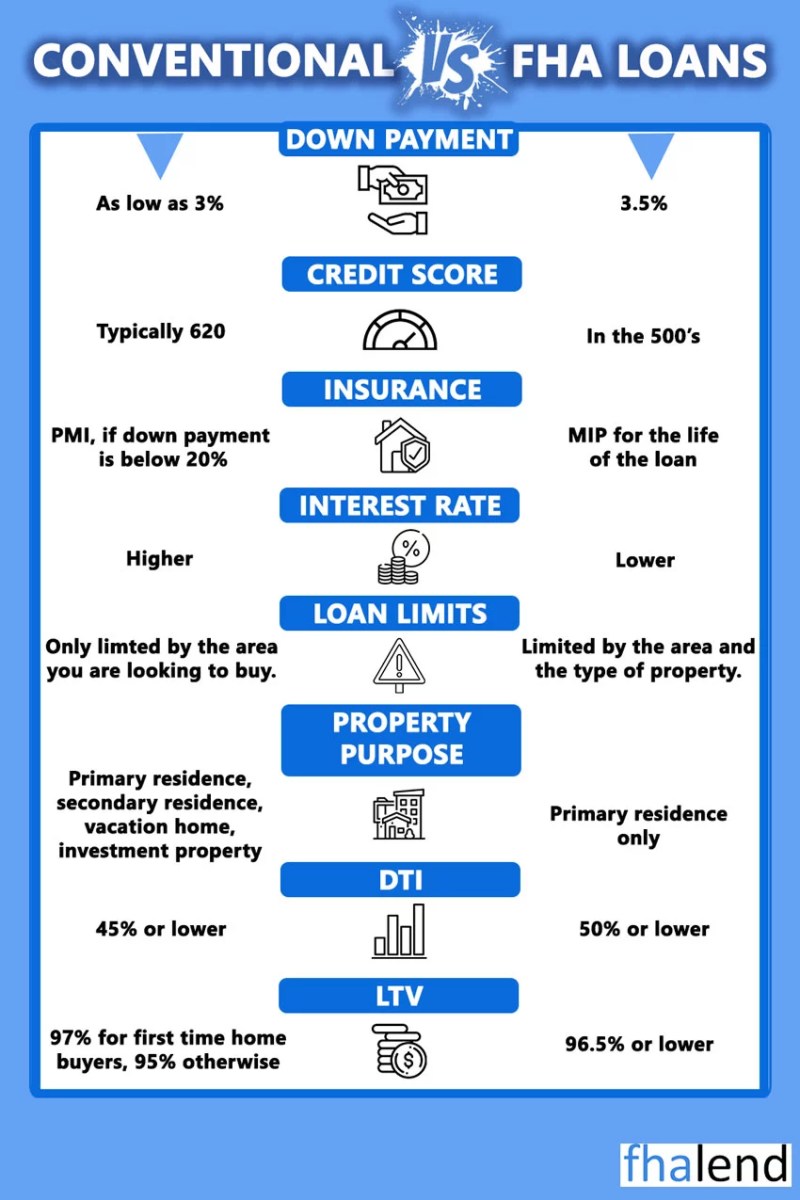

• 580+ FICO Score Up to a 96.5% LTV Buy or 97.75% LTV Rate and Term or 85% LTV Cash Out Want to buy a home, but worried about paying a large down payment or worried you won’t qualify for our homebuyer program? This is understandable and common for the everyday homebuyer. But there are also options for small to medium-sized homebuyers who dream of homeownership.

Federal Register :: Hud’s Proposed Housing Goals For The Federal National Mortgage Association (fannie Mae) And The Federal Home Loan Mortgage Corporation (freddie Mac) For The Years 2005 2008 And Amendments To Hud’s

The Federal Home Loan Mortgage Corporation, known as Freddie Mac, offers accessible and affordable homeownership programs. Specifically, Home Possible® Mortgage is designed to address the needs of struggling homebuyers. We offer a variety of benefits, from low down payments to flexible loans.

If you’re a single parent looking to buy a home or are having trouble qualifying for a home loan, Freddie Mac’s Home Possible® mortgage is a great option.

Home Possible® mortgages apply only to residential home purchases. This means no vacation homes or rentals.

This program allows non-resident borrowers with a loan-to-value (LTV) of 95% or less. So you can help your elderly children or elderly parents buy a home without living there.

Non Occupying Co Borrower Guidelines: Fha, Fannie Mae & Freddie Mac

The borrower’s income cannot exceed 100% of the Area Median Income (AMI) where the home is being purchased, unless the property is located in a low-income area by the Census Bureau.

There will continue to be no Affordable Home® income restrictions for properties in low-income areas where the median income is at or below 80% of AMI.

Freddie Mac’s Affordable Home® Mortgage does not include any non-loan financing. However, boarder income is also included. So, if you’ve lived with someone for at least a year and they’ve paid you rent, you can count that as income.

Home Possible® Mortgage has training requirements. To qualify for the program, borrowers must complete training or instruction from an approved provider.

A First Look At The Cash Window

However, if one of your borrowers is not a first-time homebuyer, they can skip the training. If you want or need tips on homeownership, you can get them for free online in Freddie Mac’s CreditSmart® Tutorials.

Additionally, there are many local first-time homebuyer classes that can help you navigate the mortgage and homebuying process. Use our search tool to find a list of local courses near you.

HomeReady® and Home Possible® loan programs have lower credit score requirements than FHA loans. However, a small amount of mortgage insurance, which you can purchase when your home equity reaches 80%, can save you a lot of money compared to a 15 or 30-year mortgage.

Everyone deserves the opportunity to own their own home. The Affordable Home® Mortgage is an excellent option for homebuyers who can’t afford a 20% down payment or have a credit score of 700 or higher. Embrace the American dream of homeownership and it will be yours!

Freddie Mac Mortgage Guidelines On Conventional Loans

Our team of experts will guide you in finding a loan that will save you money. Have you ever wondered how you can help a family member or close friend buy a home even if you don’t want to live there? This is where FHA loans and non-resident borrowers come into play. This article aims to provide a comprehensive guide to this topic. Let’s jump in!

First, FHA loans are Federal Housing Administration loans designed to help low-income, low-credit, or first-time homebuyers secure a home. These loans are federally insured, have lower down payment requirements than traditional loans, and are much easier on your credit score. But what if you still can’t be alone? This is where co-borrowers come into play.

A co-borrower is another person who applies for a loan along with the original borrower. A borrower’s income, assets, and credit score are all considered when determining loan eligibility. But did you know that there are different types of loans? For FHA loans, there is a special type called non-resident borrowers.

A non-resident borrower is a person who signs the loan documents and assumes financial responsibility for the loan but does not reside in the area. The most common candidates are parents, close friends, or other family members.

High Debt To Income Ratio Mortgage Loans

Having a non-resident borrower can provide benefits, such as increasing your loan amount or improving your eligibility. However, this system also has disadvantages, such as sharing the financial burden.

Lenders typically look for financial stability and a credit score of around 500. Although the exact criteria may vary, both first-time and non-resident borrowers must have a stable income and acceptable credit.

Stable income will be income/employment within the last two years and the ability to provide evidence of current employment.

As a non-resident borrower, it is important to understand that your name is not just your name on a piece of paper. You provide both financial and legal services.

Freddie Mac’s Home Possible Loan: 2023 Eligibility & Faqs

First home buyers and low income earners often use non-residential lenders. These situations often require additional cash replenishment, and this is where non-cohabiting borrowers come in.

Non-resident borrower retention is often used when the primary borrower has unexpected income or a high debt-to-income ratio.

The lender will send both you and the borrower a complete credit report for review and electronic signature.

Pay close attention to the loan estimate, which breaks down expected payments, closing costs, escrow (for taxes and insurance), and loan terms.

Freddie Mac Home Possible Mortgage

Let’s think about Mark and his mother, Kim, who successfully found Mark’s first home using this method. This case illustrates how a non-resident co-borrower can induce a homeowner to foreclose.

Mark is an ordinary teenager striving for the cornerstone of the American dream: homeownership. He is taking on financial responsibility with secured loans, but there are hiccups. His main source of income is based on tips, which he earns under the table at the restaurant where he has been a loyal employee for three years. While this may give him flexibility and strong cash flow, it presents a hurdle when it comes to securing a home loan.

His prospective lenders were confident in Mark’s prospects but suggested a lack of tangible cash could be a make-or-break factor. This is where non-resident borrowers can scale.

Mark did not hesitate to report this problem to his parents. Together, the family recognized the importance of Mark owning assets at his age, especially considering the long-term benefits such as wealth accumulation and tax incentives. Mark’s mother, Kim, appeared to be the perfect candidate as a non-resident borrower. He has a strong financial history, has little debt, and is interested in Mark’s financial future.

Mortgage Co Borrowers Vs. Co Signers

Kim’s financial resources provided the necessary yin to Mark’s yang. He was able to ensure Mark’s financial performance in a way that met the lenders’ requirements. This method of pooled borrowing is not new. Sponsored by FHA

Fannie mae non occupant co borrower, non occupant co borrower cash out refinance, fha non occupant co borrower, freddie mac non occupant co borrower cash out refinance, non occupant co borrower, freddie mac non occupant co borrower refinance, non occupant co borrower conventional loan, freddie mac non occupant co borrower guidelines, non occupant co borrower conventional, fannie mae non occupant co borrower guidelines, usda non occupant co borrower, non occupant co borrower fha guidelines