Insurance Policy Adalah – Insurance 4 Simple Steps to Manage Your Insurance Policy Have you completely forgotten about the insurance policy you bought ten years ago from an agent who was not in the insurance industry? Here is a 4-step process to recover all your important details.

Except for the fact that they both have bombs, you probably forgot about them long ago and probably kept them in a dark corner of your house.

Insurance Policy Adalah

Note: Before you begin, it may be helpful to create a spreadsheet documenting the different types of policies and their details.

Why Do We Pay For Healthcare Insurance When It Won’t Even Cover The Cost Of Routine/preventive Care?

The first step to understanding your insurance policies is to know what they are first. For that we need to know what types of politics there are. Most policies can be classified into one of the 7 categories below.

But how do you know what type of insurance your policy belongs to? For your convenience, here is a simple description of the different types of policies.

Plain vanilla insurance covers you for a fixed term (usually up to age 65) and has no cash value.

Insurance that covers you for life. It has a savings/investment component that accumulates cash value.

Insurance Pro Offers A Wide Range Of Life Insurance Policies

Offers unlimited investment and protection. Insurance premiums are deducted via units in the funds.

Pay if you are arrested and need surgery. Usually their policy has the word “shield”.

Paid if unable to work due to a disability. See the list of disabled people in the policy document

Pays fixed amount in case of serious accident. Payment terms are specified in the program documents.

Mutual Insurance Company: Definition And How They Invest

Note: The policy type must be the second column after the name in the first column in your spreadsheet.

Once you know the type of policy, you need to know what the policy covers and the payout amount in case of any claim.

Note that some plans are accelerators. In other words, when one point (for example, critical illness) is activated, cover for another point (for example, death) stops. It is important to document it.

Note: If you are using a spreadsheet, the coverage type and payment amount must be in the third and fourth columns.

What Is Non Life Insurance Policy?

This is a very important step for managing insurance policies. You don’t want to see a huge sum because the policy lapsed only to realize you can’t claim for it.

Consider the term of the policy and how long the coverage will last. Whole life insurance plans, hospitalization and surgical plans have no policy term and continue as long as you pay the premiums.

Next, you need to know the premium payment conditions. Check if you are paid monthly, quarterly, semi-annually or annually. This is important so you don’t miss a payment due to insufficient funds in your bank account, as this results in policy lapses.

Note that the policy term (how long the cover is kept) and the payment term (how long you have to pay premiums) may not be the same.

How Insurance Works?

Once you have all the information, you can estimate the total coverage for different events. Here you can smell some kind of mistake. As you grow, so do your needs, and your insurance may not be enough.

This is a PolicyPal guest post if you’re having trouble managing your policy. Simply upload photos of your policy and coverage information will be displayed in an overview, as well as an independent comprehensive review of your policy! An insurance policy can protect you against common life hazards, from flood and fire to car accidents and life. dangerous diseases. You cannot stop accidents, but a good insurance policy can finance these unexpected expenses.

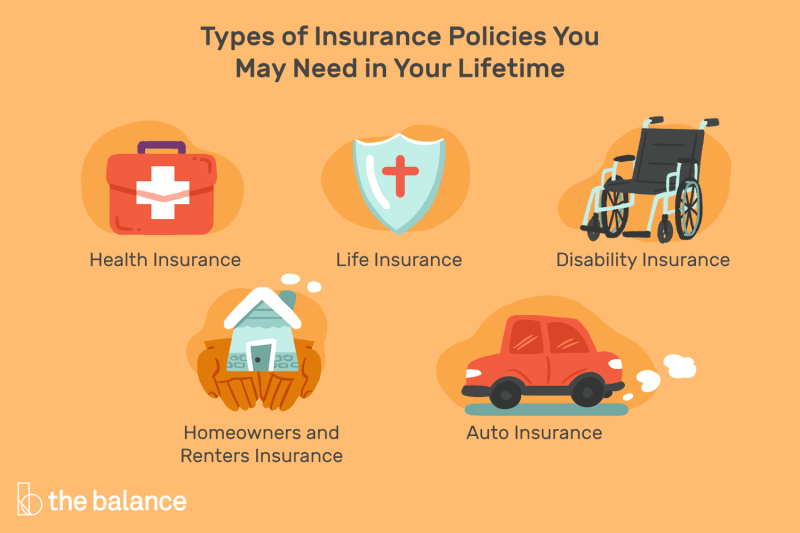

Protecting your most important assets is an important step in creating a personal financial plan, and the right insurance policy can help protect your income and assets. In this article, we discuss five policies that you should not do without.

The prospect of long-term disability (LTD) is so terrifying that some people ignore it. While we all think “nothing will happen to me,” it is not a good idea to rely on hope to protect your future income. Instead, choose a disability policy that provides enough coverage to enjoy your current life, even if you can no longer work.

Things To Consider Before Choosing The Right Travel Insurance Policy

Long-term disability provides cash benefits equal to a portion of the insured’s wages (for example, 50% or 60%) for a covered disability. Long-term disability usually begins after short-term disability ends. In order to receive benefits, the disability must occur after the policy is issued, and then usually after a waiting period. Normally, medical information certified by a doctor must be submitted to the insurer for review.

Most long-term disability insurance policies categorize disability as an occupation or some occupation. Occupational disability refers to the insured’s inability to perform his or her usual work or similar work due to a disability. Any occupation means that the insured cannot perform the job for which they are qualified because of their disability.

Similar to short-term and long-term disability insurance, worker’s compensation or worker’s compensation, it pays cash benefits to workers who are injured or disabled on the job or in the workplace. Most states require employers to carry workers’ compensation insurance for their employees. Instead, employees cannot sue their employer for negligence.

While long-term disability insurance and workers’ compensation insurance pay for disability, long-term disability insurance is not limited to disabilities or injuries that occur on the job or while working.

A Guide To Life Insurance Policy And Its Benefits

Life insurance protects people who depend on you financially. If you die, your parents, spouse, children or other loved ones experience financial difficulties, then life insurance should be high on the list of mandatory insurance policies. Think about how much income you will earn each year (and how many years you plan to work) and buy a policy to replace that income in the event of your untimely death. Funeral expenses are a factor, as unexpected expenses are difficult for many families.

The rising cost of health care is reason enough to make health insurance a necessity. Even a simple visit to the GP can add up to a big bill. Serious injuries that result in hospitalization can run up a bill that exceeds the price of a week’s stay at a luxury resort. Injuries that require surgery can quickly rack up five-figure costs. While the cost of health insurance is a financial burden for everyone, the potential cost of not having coverage is much greater.

Changing your home is an expensive proposition. Having the right home owner’s insurance can make the process less difficult. When youare shopping for a policy, look for a policy that covers structural and contents replacement in addition to living expenses while your home is being repaired.

Remember, the cost of remodeling doesn’t have to include the value of the land because you own it. Depending on the age of your home and its amenities, the cost of replacing it may be more or less than what you paid. To get an accurate estimate, find out what local builders charge per square foot and multiply that number by the amount of space you need to replace. Don’t forget to factor in the cost of upgrades and special features. Also, the policy should cover the costs of liability for injuries that may occur to your property.

Learn How To Use The Naic Life Insurance Policy Locator

Tenants also need peace of mind that they will be made whole in the event of a loss. Fortunately, renter’s insurance is one type of insurance that is available to people who rent or lease property. This insurance provides coverage for personal property, liability and additional living expenses for covered losses.

There can be two types of property coverage for a property: homeowners insurance and renters insurance. Homeowners insurance, however, does not cover a renter’s personal property. That’s why it’s important for renters to get renters insurance to protect their property.

Although renters insurance is different from homeowners insurance, they have the same components: A coverage for residence, B for other structures, C for personal property, D for additional living expenses (also known as loss of use), E for liability, and F for medical payments. for a. Because renters are not responsible for home or other structure insurance, A and B coverages are often set at $0.

:max_bytes(150000):strip_icc()/Unit-linked-insurance-plan-resized-d9ca6fd160504191b77aee8d2c1b9fec.jpg?strip=all "Insurance Policy Adalah")

Coverage C covers the tenant’s personal property. Cover D provides additional benefits for living expenses in the event of a loss. For example, if a tenant moves out of the house due to a fire, cover D covers the costs of living elsewhere, such as hotel and food costs. Coverage E covers injuries and property damage caused by the insured, while coverage F covers medical expenses.

Planning To Buy Life Insurance Policy? First Understand These 7 Terms For Perfect Purchase

Commercial policy insurance, business owners policy insurance, insurance adalah, insurance-policy, pet insurance policy, buy life insurance policy, liability insurance adalah, business policy insurance, insurance policy, best life insurance policy, cyber insurance policy, level term insurance policy