Examples Of Operational Risk Management – We believe that a strong culture of risk-taking is essential to the long-term success of a business banking franchise. This ensures that our decisions and actions are considered and focused on our customers, and that we are not swayed by perceived short-term benefits. Specifically, risk culture refers to the practices, attitudes and behaviors related to risk awareness, risk taking and risk management, and the controls that govern risk decision making*. At UOB, our risk culture is based on our values.

Managing risk is critical to how UOB creates long-term value for our customers and stakeholders. Our risk culture is based on four principles: implementing strong risk governance; balancing growth and stability; ensuring accountability for all our risk-based decisions and actions; and promote awareness, commitment and sustainable behavior among every employee. Each of these policies is based on UOB’s unique values that guide every action we take. As we strengthen our culture of risk-taking throughout our franchise, we maintain our commitment to financial security and integrity; Correct results and correct support for our customers; A sustainable and prudent business practice and operation based on integrity, ethics and morality.

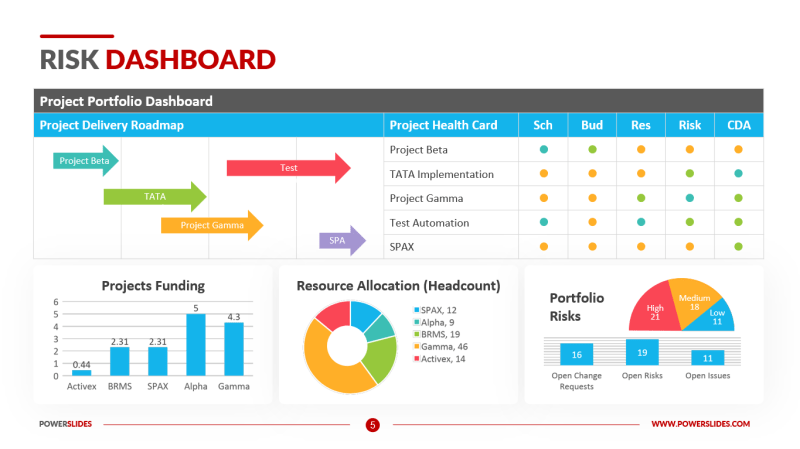

Examples Of Operational Risk Management

UOB’s risk management structure, as shown in the following figure, highlights the Group’s risk culture. Under the structure, various functions of risk management and control work with businesses and support groups to identify their risks and to facilitate their risks and manage their self-assessment.

The New World Of Risk—and What To Do About It

Our risk management strategy aims to incorporate our risk culture to help identify, manage and mitigate ongoing risks due to factors external to our business activities and to use adequate capital to deal with them. and these risks. Risks are managed within the framework established by the senior management committees and approved by the Board and its committees. We have developed a set of policies, procedures, tools and processes that will enable us to identify, measure, monitor and manage the material risks facing the Group. This enables us to focus our efforts on banking fundamentals and create long-term value for all our stakeholders.

The Group’s risk management framework, policies and appetite provide principles and guidance for the Group’s risk management activities. They help to shape our key decisions for financial management, strategic planning and budgeting and operational management to ensure that the level of risk is properly and accurately considered. In particular, the group’s internal capital adequacy assessment process (ICAAP), which includes stress analysis, takes into account the group’s risk appetite to ensure that the group’s capital, risk and returns are acceptable under the circumstances different stressors. We also take into account the group’s risk appetite in the development of key risk indicators (KPIs) for measuring performance. It works to create a risk culture and risk management mindset throughout the organization.

Our risk identification, assessment, monitoring and reporting processes are governed by our effective risk management plans, policies and aspirations. Risk reports are presented regularly to management and the Board to inform them of the Group’s risk profile.

UOB’s responsibility for risk management begins with the Board overseeing a governance structure designed to ensure that the Group’s business activities:

Risk Management In Banking: Types + Best Practices For Mitigation

In this regard, the Board is mainly assisted by the Board’s Risk Management Committee (BRMC). The BRMC assesses the overall risk appetite and level of risk capital to be retained by the Group.

The CEO has established senior management committees to help him make business decisions by taking into account the appropriate risks and rewards. The main management committees involved are the Executive Management Committee, the Risk and Capital Committee, the Assets and Liabilities Committee, the Credit Committee and the Risk Management Committee. These committees also assist the board committees in certain risk areas.

Management and executive committees are authorized to set risk appetite limits based on geographic, business segments and/or broad products.

:max_bytes(150000):strip_icc()/operational_risk.asp-Final-4be32b4ee5c74958b22dfddd7262966f.png?strip=all "Examples Of Operational Risk Management")

Risk management is the responsibility of every employee within the Group. Risk awareness and responsibility are embedded in our culture with a formal framework that ensures appropriate oversight and accountability for effective risk management across the Group and risk types. This is done through a corporate governance structure that provides three “lines of protection” as follows:

How I Used Chatgpt To Create A Risk Taxonomy For Generative Ai In Just One Hour

Business and support functions have primary responsibility for implementing and implementing effective controls to manage risks arising from their business activities. This includes establishing adequate management and leadership controls to ensure compliance with risk policies, appetites, limits and controls, and highlighting regulatory gaps, process inadequacies and risk events that were unexpectedly.

Risk management and control functions (group credit and risk management, and group compliance) and the chief risk officer provide a second line of defense.

The risk monitoring and control function supports the Group’s strategy to balance growth and stability by establishing a risk framework, strategies, appetite and boundaries within which business activities must operate. The Risk Monitoring and Control function is also responsible for independently reviewing and evaluating the Group’s risk profile and highlighting any significant weaknesses and risk issues to the relevant Management Committees.

The independence of risk management and control functions from business processes ensures that the necessary checks and balances are in place.

Operational Risk Management Structure In Financial Companies Three Line Of Defense Model Defining Key Accountabilities Template Pdf

The Group’s internal and external auditors carry out risk-based audits covering all aspects of the first and second level of security to provide independent assurance to the CEO, the Audit Committee and the Board on the effectiveness of controls of risks and regulatory structure, policies, strategies . , systems and methods.

The Group’s management framework also provides oversight for our foreign banking subsidiaries in a matrix reporting structure. Our departments, in consultation with the Group Risk Management, adjust the governance structure, planning and policies in line with local regulatory requirements. This ensures that the approach is consistent across the Group and is flexible enough to suit the local operating environment.

UOB has developed a risk appetite framework to define how much risk we are able to take and how much risk we are willing to take to achieve our business objectives. The purpose of creating an appetite plan is not to reduce risk-taking, but to ensure that the group’s level of risk remains within well-defined and tolerable limits. The plan has been developed based on the following key points:

Risk appetite defines appropriate boundaries and limits in key areas, including, but not limited to, credit risk, country risk, market risk, liquidity risk, operational risk and risk of fame. Our risk approach focuses on businesses that we understand and are well equipped to manage the risks involved. In this way, we aim to reduce earnings volatility and concentration risk and ensure that our high credit ratings, strong liquidity and financial base remain intact. This enables us to be a reliable partner to our customers through changing economic conditions and cycles.

Top 10 Operational Risk Management Software In 2024

UOB’s risk appetite framework and risk appetite are reviewed and approved annually by the Board. Directors monitor the risk profile and risk appetite and report to the Board.

UOB’s business strategies, products, customer profile and operating environment expose us to a number of financial and non-financial risks. Identifying and monitoring significant risks is an important part of the Group’s approach to risk management. This helps us to properly assess and mitigate these risks to the Group. The following table lists the main risks that may affect the achievement of the Group’s strategic objectives:

The risk of loss arising from the failure of a borrower or counterparty to meet its financial obligations when such obligations become due.

The probability of default/loss is considered in the group’s credit risk management plan, strategies, default/portfolio model and default/exposure limits.

Enterprise Risk Management

Risk of loss to the Group due to fluctuations in market conditions or underlying asset prices (such as changes in interest rates, foreign exchange rates, equity prices, commodity prices and spreads when credit). This includes interest rate risk in the banking book which is the potential loss of income or reduction in earnings due to changes in the interest rate environment.

With the Group’s market risk management plans, policies, risk assessment models and limits. Interest rate risk in the banking book is managed through the Balance Sheet risk management framework, and interest rate risk is managed in the rules and limits of the banking book system.

The risk caused by the group’s inability to fulfill its obligations or funds increases in assets when necessary.

Risk of loss resulting from inadequate or failed internal processes, people and systems or external events. Potential losses may be financial loss or other damage, for example, loss of reputation and public confidence which may affect the bank’s credibility and its ability to make transactions, save money and get new business . This includes banking operational risk, fraud risk, legal risk, redundancy risk, regulatory risk, reputational risk and technology risk.

Fm3 21.91 Appendix B

With relevant risk management methods, strategies, critical risk assessment and control, key performance indicators of risk and incident management.

Current or potential adverse effects on earnings, revenue or reputation resulting from poor strategic decisions, improper decision-making processes or lack of response to industry, economic or technological changes.

Adverse effects on earnings or revenue resulting from changes in business conditions such as volume, volatility and costs.

This is a risk caused by the use of the model

Pdf] The Use Of Key Risk Indicators By Banks As An Operational Risk Management Tool: A South African Perspective

Operational risk management jobs, operational risk kri examples, examples of operational risk events, rcsa operational risk examples, operational risk management framework, operational risk metrics examples, operational risk controls examples, operational risk events examples, operational risk banking examples, operational risk management examples, operational risk management, examples of operational risk