Additional Student Loans For Living Expenses – If youare a recent graduate or college graduate, you may be surprised at how much of your monthly student loan payment goes toward just the interest portion of your loan. To understand why that is, you must first understand how that interest is generated and how it is applied to each payment. You can do this by calculating it yourself and digging deeper into your student loan balances and payments. To calculate your student loan interest rate, calculate the daily interest rate, then identify your daily interest rate, then convert it to a monthly interest payment. From there, you’ll have a better idea of what you’ll pay each month.

Understanding how lenders charge interest for a particular billing cycle is actually quite simple. All you have to do is follow these three steps:

Additional Student Loans For Living Expenses

You first take the annual interest rate on your loan and divide it by 365 to determine the interest compounded daily.

Refinancing Student Loans: Who Should Do It

Say you owe $10,000 at 5% annual interest. You would divide that 5% rate by 365: 0.05 ÷ 365 = 0.000137 to arrive at a daily rate of 0.000137.

Then multiply your daily interest rate in step 1 by your outstanding amount. Let’s use the $10,000 example again for this calculation: 0.000137 x $10,000 = $1.37

This is $1.37 in interest that you will be assessed per day, which means you will be charged $1.37 in interest per day.

Finally, you need to multiply that daily interest amount by the number of days in your billing cycle. In this case, we will assume a 30-day cycle, so the amount of interest you pay for the month is $41.10 ($1.37 x 30). A total of $493.20 per year.

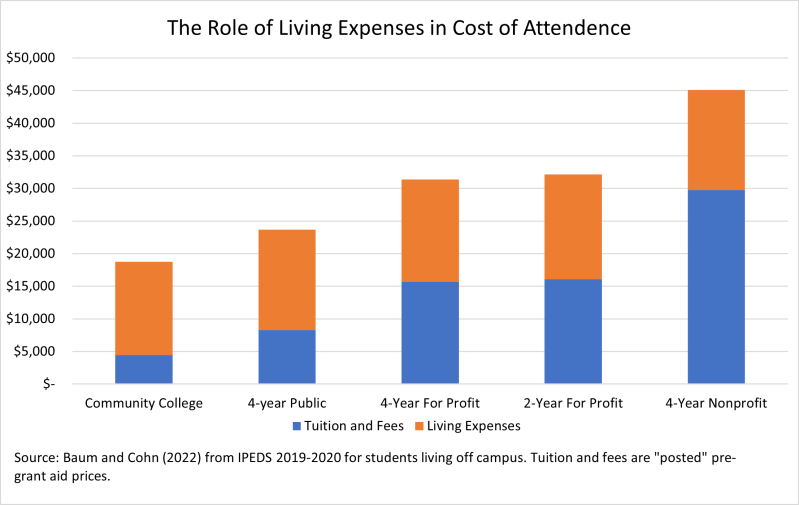

Cost Of Attendance

This is how interest begins to accrue from the time your loan is paid until you have a federally forgiven loan. In that case, you will not be charged interest until after the six-month grace period after you open the school.

With unsecured loans, you can choose to pay any accrued interest while you’re still in school. Otherwise, the accrued interest is capitalized after graduation, or added to the principal amount.

If you and are granted a deferment – a pause on your loan repayments, usually for around 12 months – keep in mind that all your payments will also stop while you are in forbearance, interest to continue to go during that period. and will ultimately be charged to your principal amount. If youare experiencing financial hardship (including unemployment) and are in foreclosure, only if you have an unsecured or PLUS loan from the government.

Student loan payments are suspended and 0% interest has been imposed throughout the COVID-19 pandemic. This is still true as of February 2023, but could change if the first of two things happens: 60 days pass after the student loan forgiveness plan is allowed to be implemented or the case is settled; or 60 days after June 30, 2023.

Cost Of Living Crisis To Hit Students Harder Than Expected

The calculation above shows how interest payments are calculated based on what is known as the simple compound interest formula; This is how the US Department of Education handles federal student loans. With this method, you only pay interest as a percentage of the principal balance.

However, some private loans use compound interest, which means that the daily interest is not added to the principal amount at the beginning of the billing cycle – it is added to the remaining principal amount.

So on the second day of the billing cycle, you don’t apply the daily interest — 0.000137, in our case — to the $10,000 in principal you started the month with. You multiply the daily rate by the principal and the amount of interest accrued the previous day: $1.37. It works well for the banks because, as you can imagine, if they screw up like that, they collect more interest.

The above calculation also includes a fixed interest rate over the life of the loan, which is what you would have with a federal loan. However, some private loans come with variable rates, which can go up or down depending on market conditions. To determine your monthly interest payment for a given month, you must use the current rate charged on the loan.

How Can Student Loans Affect My Credit

Some personal loans use compound interest, which means that the daily interest rate is multiplied by the principal amount of the additional month.

If you have a fixed-rate loan – either through the Federal Direct Loan Program or a private lender – you may find that your monthly payment stays the same, even though the remaining principal, and thus the interest cost, decreases each month . to the other.

This is because these borrowers pay, or pay together, during the repayment period. If the interest portion of the bill goes down, the principal amount you pay each month increases by a corresponding amount. Therefore, the total bill remains the same.

The government offers a number of income-driven payment options designed to reduce payment amounts initially and gradually increase them as your wages increase. At first, you may find that you are not paying enough on your loan to cover the amount of interest that accrues each month. This is what is known as “negative amortization”.

Compare Private Student Loans

With some plans, the government will pay all, or at least part, of the uncovered interest. However, with the income required payment plan, unpaid interest is added to the principal each year. Keep in mind that once your remaining loan balance is 10% higher than your original loan amount, that principal is gone.

The more money you pay toward just the principal balance of your student loans, the less interest you will pay over the life of the loan. However, it is not always possible. If you can’t afford to pay off your student loans every month or year, you may want to see if you can refinance your student loans to get a lower interest rate.

Refinancing isn’t always ideal because it can cause you to lose some of the protections offered by federal student loans. But, if you have private student loans, refinancing can help you get a lower interest rate. Consider the best student loan restructuring companies and then decide what is best for your financial situation.

Interest rates on federal student loans are set by federal law, not the US Department of Education. They are based on the 10-year Treasury yield, with an additional rate added.

Student Loan Payment Pause Benefits High Income Households The Most

It depends. Debt consolidation can make your life easier, but you have to do it carefully so that you don’t lose the leverage you currently have among the debts you have. The first step is to find out if you are eligible to file a claim. You must be enrolled in less than part-time status or not in school while currently making loan payments, or be in and out of the loan period.

Yes. Individuals who meet certain criteria based on filing status, income level, and the amount of interest paid can deduct $2,500 from their taxable income each year.

Figuring out how much you owe in student loan interest is a simple process—at least if you have a standard payment plan and a fixed interest rate. If you want to reduce your total interest payments over the course of the loan, you can always check with your credit servicer to see how different payment plans affect your costs.

Requires authors to use primary sources to support their work. These include white papers, government data, original reports, and interviews with industry experts. We also include original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing fair and unbiased content in our editorial policy.

Step 4: Resolve Your Account Balance And Access Funds For Living Expenses

The offers shown in this table are from affiliates who receive compensation. These fees may affect how and where listings appear. does not include all offers available on the market. After deducting tuition and room and board from the student loan, you can use the remaining amount on optional living expenses, as they are usually part of the total approved cost of attendance. Some of the costs included are housing, rent, books and supplies, transportation, and groceries.

Each university annually calculates the cost of attendance for a range of students and is the maximum that students can borrow that year. The total cost of attendance typically includes the cost of tuition, housing, rent, room and board, books and supplies, and transportation. Necessary personal expenses such as groceries and toiletries are also often considered and are all covered by most student loans.

When you apply for any student loan, money is paid directly to your college to cover the cost of your tuition, and room and board for on-campus students. The remaining funds are then normally distributed to the student who may use them to cover their approved school living expenses.

The federal aid for which a student is eligible is equal to their financial need minus their college cost of ownership (COA).

Forgiving Student Loans: Budgetary Costs And Distributional Impact — Penn Wharton Budget Model

Taking out student loans for living expenses, extra student loans for living expenses, student loans for housing and living expenses, graduate student loans living expenses, using student loans for living expenses, student loans to pay for living expenses, private student loans for living expenses, student loans for living expenses, graduate student loans for living expenses, best student loans for living expenses, student loans for living expenses reddit, student loans to help with living expenses